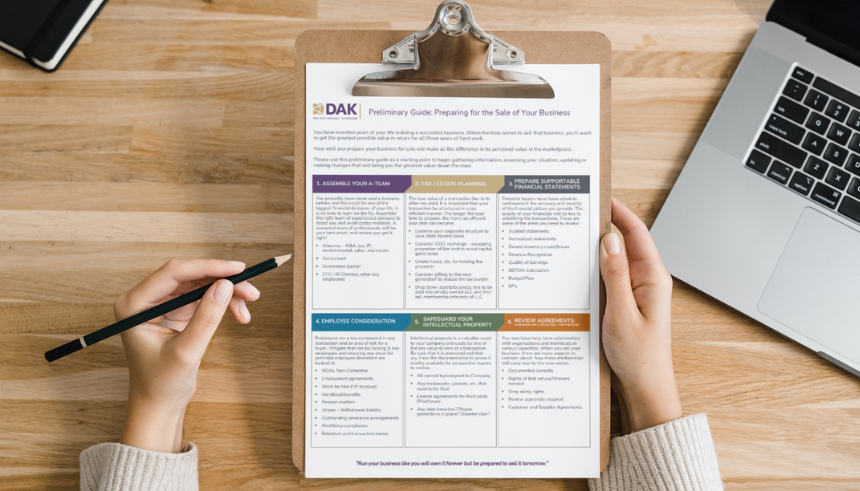

If selling your AV integration business is a thought, consider the difference between financial buyers and strategic buyers.

When a Commercial Integrator begins contemplating the sale of their AV integration business, they should be aware that there are options as to “who” will make the best buyer for their AV business.

Financial buyers (i.e. private equity, venture capital) and strategic buyers continue to be very acquisitive and interested in the AV integration sector. The best transaction partner will ultimately depend on the needs and desires of the owner.

Here is an overview of each, as well as key considerations to factor in when making a decision.

Financial Buyers

While financial buyers typically include private equity, venture capital, hedge funds and family investment offices, it is the private equity buyer that has been most active in the AV integration sector.

Private equity sponsors typically employ a buy-to-sell approach. The growth of the private equity sector is predicated on its standard practice of buying businesses and then, after steering them through a transition of performance improvement and add-on acquisitions, selling them. This is at the core of private equity’s success.

Private equity funds will generally fund an acquisition with a combination of equity and third-party debt and then steer the AV business through a transition of performance improvement, organic growth and add-on acquisitions.

On average, private equity firms will hold their investment between three and five years, then either sell to a larger private equity firm, strategic buyer or, if the company is large enough, through an Initial Public Offering.

In today’s market, private equity firms are interested in the AV integration industry for several reasons.

First, the sector is experiencing growth driven by continued innovation in technology and the rise of IT-centric unified communications positions. Second, the industry is highly fragmented, providing exceptional opportunities for value-add bolt-on acquisitions.

And thirdly, the rising importance of managed services and associated recurring revenue streams (valuation multiples are substantially higher for businesses that can demonstrate recurring revenues) make the case for private equity interest and expanding valuations in the sector.

Strategic Buyers

Strategic buyers are typically larger operating companies who generally have a strategic angle when acquiring an AV business. I believe there are two types of strategic buyers – those from within the AV integration industry (internal) and those from outside it (external).

The Internal Strategic Buyer likely already has a meaningful presence in the AV integration sector and is looking for integration businesses that can be integrated into and complement their core business.

In strategic acquisitions, buyers are primarily looking for synergies from combining companies that will increase market share, expand capabilities or geography, add exposure to new and growing end markets and ultimately improve profitability. It’s a long-term buy-and-hold strategy.

While a strategic buyer can be a competitor, it is equally as likely to be in a complementary integration business or adjacent industry, these are considered External Strategic Buyers (i.e. low voltage, mechanical, IT services, etc.).

Strategic buyers from adjacent industries are increasingly seeking opportunities to enhance relationships with their enterprise customers by offering highly complementary integration services.

Customers increasingly prefer one vendor for their AV/IT needs, or as I like to call it, the one-throat-to-choke model.

While financial buyers are primarily focused on the financial metrics, sellers can maximize the value of a transaction by getting buyers focused on things beyond the numbers to the overall value the company can bring to the acquirer in the short-term and long-term.

Sellers can maximize the value of a transaction by getting buyers focused on things beyond the numbers to the overall value the company can bring to the acquirer in the short-term and long-term…

As a result, strategic buyers generally can and will pay more for an integration business than a financial buyer.

Over the last five years, about 65% of our sell-side transactions have been sales to strategic buyers. While financial buyers were also often in the mix, during the process, the highest valuations and the least risks were in sales to strategic buyers.

If you have questions about what type of buyer might be right for your AV business, please feel free to reach out to me at afuchs@dakgroup.com.

CLICK BELOW FOR:

PRINTABLE VERSION![]() READ ORIGINAL

READ ORIGINAL